Getting through the financial trajectory with bad credit loans can feel like an uphill battle. According to the Federal Reserve, about 30% of Americans have a credit score below 670, placing them in the “bad credit” category. Despite these challenges, securing a loan with bad credit isn’t impossible!

Whether you’re facing unexpected medical expenses, need to consolidate high-interest debt, or require funds for a major purchase, various lenders offer solutions specifically designed for borrowers with credit challenges. Understanding your options for bad credit loans and knowing how to get one can help you make informed decisions and find the financial support you need without falling prey to predatory lending practices.

Understanding Bad Credit Loans and Their Purpose

Bad credit loans provide important financial access to individuals whose credit history might otherwise prevent them from qualifying for traditional financing. These specialized lending products typically come with adjusted terms to accommodate higher lending risks while offering borrowers the opportunity to address immediate financial needs and potentially rebuild their credit through responsible repayment.

What Are Bad Credit Loans?

Bad credit loans have been a financial lifeline for millions of Americans struggling with credit challenges. Trust me, I’ve been there. Years ago, when my credit score took a nosedive after some poorly timed medical bills and a job loss, traditional lenders wouldn’t even look at my application. That’s when I discovered the world of bad credit lending options — and it’s changed dramatically since then.

These specialized financial products are designed specifically for borrowers with credit scores that make conventional lenders run for the hills. Generally speaking, we’re talking about FICO scores below 580, though some lenders set their “bad credit” threshold at 620 or even 650.

But why do lenders care so much about these three-digit numbers anyway? It’s all about risk assessment. Your credit score serves as a numerical snapshot of your borrowing history and financial reliability.

Lower scores signal to lenders that you’ve had trouble repaying debts in the past. The system isn’t perfect — far from it — but it’s the measuring stick that most financial institutions use.

What makes bad credit loans different from their conventional counterparts is pretty straightforward. They typically come with higher interest rates to offset the increased risk the lender takes on. They might require security in the form of collateral or a co-signer. And you’ll often find lower borrowing limits and more restrictive terms.

These loans commonly address situations like:

- Emergency medical expenses not covered by insurance

- Critical home or vehicle repairs

- Consolidating high-interest debt

- Covering essential bills during income gaps

- Funding unavoidable major purchases when savings aren’t sufficient

According to data from the CNBC, approximately 34.8% of Americans fall into the “subprime” credit category. That’s over 64 million people potentially seeking alternative lending options. You’re not alone if you’re exploring this path.

Is a bad credit loan ideal? Nope. Is it sometimes the most realistic option when you’re in a tight spot with damaged credit? Absolutely. The key is understanding exactly what you’re getting into and using these products strategically rather than as a long-term financial solution.

Types of Bad Credit Loans Available

The view of bad credit lending has evolved tremendously in recent years. Back when I first needed one, options were pretty limited and mostly predatory. Today’s market offers more variety and, in some cases, more reasonable terms for borrowers with credit challenges.

1. Secured Bad Credit Loans

Secured loans were my entry point into rebuilding credit, and they remain one of the most accessible options for borrowers with significant credit issues. These loans require collateral — something valuable you own that the lender can take if you don’t repay the loan.

The most common types include:

- Auto title loans: Using your vehicle as collateral (while you continue driving it). These can be dangerously expensive with APRs sometimes exceeding 300%, but some credit unions offer more reasonable versions.

- Secured credit cards: Technically not loans, but they require a deposit that serves as your credit limit. I started with a $500 secured card that eventually converted to a regular credit card after 18 months of responsible use.

- Home equity loans: For homeowners, these use your property as security and typically offer the lowest rates among bad credit options, though they put your home at risk.

- Pawnshop loans: Leaving valuables with a pawnshop in exchange for a loan, with the option to buy back your items by paying back the loan plus fees.

The interest rates on secured loans vary wildly but generally range from 6% for home equity products to 25% for secured personal loans, and much higher for title loans and pawnshop financing.

The primary advantage is accessibility — lenders are more willing to say “yes” when they have collateral. The obvious downside is that you could lose your property if you default.

2. Unsecured Bad Credit Loans

Getting an unsecured loan with bad credit is tougher, but not impossible. Without collateral backing the loan, lenders rely more heavily on your income stability and other factors beyond your credit score.

The main types are:

- Personal installment loans: Fixed payments over a set term, typically 1-5 years. Interest rates for bad credit borrowers usually range from 18% to 36%.

- Payday loans: Short-term, high-cost loans due on your next payday. With APRs often between 300% and 700%, these should be a last resort.

- Cash advances: Borrowed against a credit card’s limit. Convenient but expensive, with high interest rates and fees that start accruing immediately.

The challenge with unsecured options is finding legitimate lenders willing to work with bad credit without charging predatory rates. Credit unions and community banks sometimes offer more flexible “credit-builder” loans with reasonable terms. Online lenders have also expanded options, with some specializing in bad credit situations.

3. Online Installment Loans

The digital lending revolution has been a game-changer for bad credit borrowers. The process of actually securing a loan online is quite easy compared to traditional methods that come with huge setbacks and failure due to a bad credit score.

Online installment loans typically offer:

- Loan amounts from $500 to $10,000

- Terms from 3 months to 5 years

- Fixed monthly payments

- Funding as fast as next business day

- Simple online applications with quick decisions

The convenience factor is huge. Many online lenders allow you to prequalify with a soft credit check that doesn’t hurt your score. This lets you see potential rates before submitting a full application.

Major online lenders like Upgrade, Avant, and OppLoans have built their business models around serving customers by conducting feedback surveys to know customers with imperfect credit. Their approval criteria often consider factors beyond your credit score, looking at income stability, education, and banking behavior.

The cost for this convenience and accessibility lies in the Interest rates, which typically range from 18% to 36% APR for bad credit borrowers, with origination fees between 1% and 10% of the loan amount often deducted from your funds upfront.

Bear in mind that, not all online lenders are created equal. The industry has its share of predatory operators alongside the legitimate companies. Always check for proper licensing, clear fee disclosure, and verified reviews before applying to avoid a story that touches the heart.

Top Lenders for Bad Credit Loans in 2025

Finding reputable lenders when your credit isn’t stellar feels like searching for water in a desert. But the lending horizon has evolved exponentially in recent years. Today’s bad credit borrowers have more legitimate options than ever before, thanks to specialized lending programs and technology that allows for more nuanced risk assessment beyond the almighty FICO score.

Let’s break down where you can actually get approved in 2025, based on real-world experience and current market analysis.

1. Traditional Banks with Bad Credit Programs

Most major banks still shy away from true “bad credit” territory, but some have dipped their toes in with specialized programs. Chase, for instance, launched their “Community Advantage” program in late 2023, offering personal loans to borrowers with scores as low as 560 if they have existing relationships with the bank.

Bank of America’s “Balance Assist” short-term loan program has expanded its eligibility requirements to include customers with credit scores in the 580-620 range. The loan amounts are modest — maxing out at $1,000 — but with APRs capped at 36%, they’re vastly better than payday loans.

Wells Fargo has their “Opportunity Loan” program that considers applicants with scores as low as 550, though approval typically requires either a long-standing banking relationship or enrollment in their credit education program.

These programs often require you to have an existing relationship with the bank. They’re also not heavily advertised — you’ll need to specifically ask about options for credit-challenged customers.

2. Credit Unions: The Silent Powerhouses

Credit unions continue to be my top recommendation for bad credit borrowers. Local credit unions are better at offering secured personal loans that can be used for rebuilding your credit score or sorting out your debt right on time.

Credit unions like Navy Federal, PenFed, and First Tech Federal have specifically designed products for members with damaged credit.

Their “Fresh Start” or similarly named loans typically offer:

- More flexible credit score requirements (sometimes as low as 500)

- Lower interest rate caps than online lenders (usually maxing out around 18-25%)

- Smaller minimum loan amounts for those who need just a little help

- Financial education resources as part of the borrowing process

Even better, many community-based credit unions offer “payday alternative loans” (PALs) with regulated terms and reasonable interest rates. These typically range from $200 to $2,000 with terms up to 12 months and APRs capped at 28%.

The downside is that you need to qualify for membership, which might be based on where you live, work, or other affiliations. And smaller credit unions may have limited digital capabilities compared to online lenders.

3. Online Lenders Specializing in Bad Credit

The online lending sector has exploded with options for bad credit borrowers. Some focus exclusively on this market, using alternative data points beyond traditional credit scores to evaluate applications.

Based on current 2025 metrics and borrower feedback, standout options include:

- Upstart: Their AI system underwriting considers factors like education and employment alongside credit scores, approving borrowers with scores as low as 580. Their rates for bad credit typically range from 19.99% to 35.99%.

- Upgrade: Offering personal loans to borrowers with scores as low as 550 with loan amounts from $1,000 to $50,000. They’ve recently improved their terms for bad credit borrowers, with rates now starting at 8.49% for secured loan options.

- OppLoans: Specializing in very poor credit situations (scores below 550), they’ve expanded their state coverage to 41 states as of early 2025. Their rates are high (typically 59%-160% APR) but still far better than payday loans.

- NetCredit: Another option for very challenged credit, offering loans up to $10,000 with terms from 6 to 60 months.

The advantage of these online platforms is accessibility — applications take minutes, decisions often come within hours, and funds typically arrive within 1-3 business days. Many also report to all three credit bureaus, helping you build credit with on-time payments.

4. Peer-to-Peer Lending Platforms

P2P lending has matured significantly since its early days. Instead of borrowing from an institution, you’re basically borrowing from individuals or groups of investors.

Leading P2P platforms that work with bad credit borrowers include:

- Prosper: Recently lowered their minimum credit score to 560, though approval at this level typically requires excellent income and low debt-to-income ratio.

- Peerform: Accepts borrowers with scores as low as 580, with loan amounts up to $25,000. Their “Creditworthy” program introduced recently specifically targets rebuilding borrowers.

- SoLo Funds: A micro-lending platform for smaller loans (typically under $1,000) that uses alternative data rather than traditional credit scores. Perfect for smaller emergency needs.

P2P lending can sometimes offer more competitive rates than traditional bad credit lenders because individual investors are making the lending decisions rather than institutional algorithms. The downside is that funding isn’t guaranteed — your loan request needs to attract enough investor interest.

5. Government-Backed Loan Programs

Don’t overlook loan programs with government backing or regulations that make them more accessible to credit-challenged borrowers:

- FHA Home Loans: For homebuyers, FHA loans accept credit scores as low as 500 (with a 10% down payment) or 580 (with 3.5% down).

- Disaster Assistance Loans: The SBA offers personal loans for disaster recovery with terms more favorable than typical bad credit options.

- Income-Based Repayment Plans: For student loans, federal programs can make payments more manageable regardless of credit score.

- Community Development Financial Institutions (CDFIs): These locally-based lenders receive federal funding specifically to serve underbanked communities, often with more flexible credit requirements.

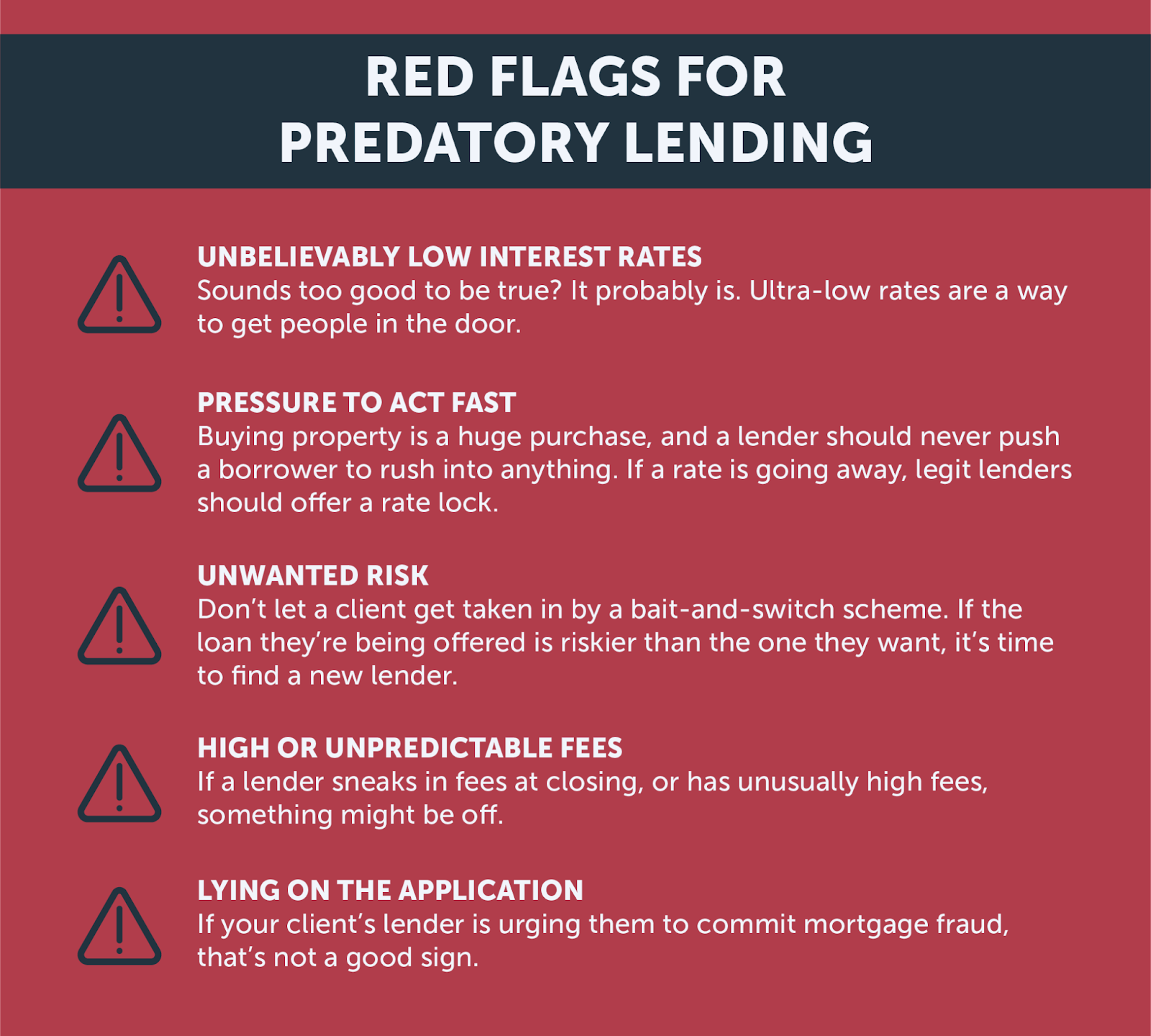

Red Flags and Predatory Lenders to Avoid

The bad credit lending space still has its share of predators.

To be safe out there you’ll need to watch out for:

- Lenders who don’t check your ability to repay at all

- Loans with APRs above 36% (except in specific short-term situations)

- Required upfront fees before loan approval

- Pressure tactics and rushed application processes

- Lenders who don’t report to credit bureaus

- Contracts with prepayment penalties or balloon payments

How to Apply for Bad Credit Loans

Getting through the application process for bad credit loans can feel intimidating, especially after facing rejection from mainstream lenders. I remember staring at my first bad credit loan application, second-guessing every answer and wondering if I was setting myself up for another disappointment. But here’s the thing: preparation considerably improves your chances.

Let me walk you through the process I’ve both personally used and helped others navigate over the years.

Before You Apply: Pre-Application Preparation

Smart borrowers do their homework before submitting a single application.

Here’s your pre-application checklist:

- Check your current credit reports and scores – Knowledge is power. Pull your free reports from annualcreditreport.com and know exactly what lenders will see.

- Calculate how much you truly need – Borrowing more than necessary means paying more interest. Break down exactly what the funds will cover to arrive at a specific number.

- Determine what you can afford monthly – Create a budget showing how a new loan payment fits in. My rule of thumb: your total debt payments shouldn’t exceed 36% of your gross income.

- Gather required documentation – Typical requirements include:

- Government-issued ID

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residence (utility bills, lease agreement)

- Social Security Number

- Banking information for deposits and payments

- Research lender requirements – Different lenders have different minimum criteria. Some care more about current income than credit history. Understanding these nuances helps target your applications effectively.

During this preparation phase, I’d also recommend writing a brief letter explaining any major negative items on your credit report (like medical collections or a past bankruptcy). Some lenders, particularly credit unions, take these explanations into consideration.

The Application Process Step-by-Step

Once you’re prepared, here’s how the actual application process typically unfolds:

Step 1: Pre-qualification (when available)

Many online lenders and some traditional lenders offer pre-qualification that uses a soft credit pull (which doesn’t affect your credit score). This gives you a preliminary answer about:

- Whether you’re likely to be approved

- Potential loan amounts

- Estimated interest rates and terms

It’s good practice starting with pre-qualification when possible to avoid unnecessary hard inquiries. When rebuilding your credit, I pre-qualified with three different lenders before choosing one for a full application.

Step 2: Formal Application Submission

The formal application will be more detailed than pre-qualification. Depending on the lender, you might complete this:

- Online through a secure portal

- Over the phone with a loan officer

- In-person at a branch location

Be completely honest on your application. Even minor discrepancies between your stated information and what appears in verification documents can lead to denial.

Step 3: Verification and Underwriting

After submission, the lender reviews your application through a process called underwriting.

This typically involves:

- Verifying your identity and documentation

- Conducting a hard credit inquiry

- Assessing your debt-to-income ratio

- Evaluating your employment stability

- Checking your banking history (especially for online lenders)

This phase can take anywhere from minutes (with automated online systems) to several days (with traditional banks or for larger loans).

Step 4: Loan Offer and Agreement

If approved, you’ll receive a loan offer detailing:

- Approved loan amount

- Interest rate and APR

- Repayment term and monthly payment

- All fees and charges

- Disbursement method and timeline

This is your last chance to review all terms before accepting. it’s very necessary to take your time here! The clause could be about bi-weekly rather than monthly payments, which could pose as a funding problem in the future.

Step 5: Acceptance and Funding

After accepting the offer and signing the loan agreement (usually electronically), funding follows. The timeline varies by lender:

- Online lenders: Often 1-3 business days

- Credit unions and banks: Typically 2-7 business days

- P2P platforms: Can take up to 7-10 days as investors fund your loan

Some lenders offer same-day or next-day funding for an additional fee. Whether this is worth it depends on your urgency.

Common Reasons for Bad Credit Loans Denial and How to Overcome Them

Getting rejected is discouraging, but understanding why helps you improve your next application. Common reasons include:

- Insufficient income relative to the loan amount: Consider applying for a smaller loan or adding a co-signer.

- Too many recent hard inquiries: Wait 3-6 months before applying again while working on your credit.

- Unstable employment history: If possible, wait until you’ve been at your current job for at least six months.

- High debt-to-income ratio: Work on paying down existing debts before reapplying.

- Insufficient banking history: Open a checking account and maintain it in good standing for at least 3 months.

- Recent Overdue debts or collections: Make arrangements to resolve them or wait until they’re at least 12 months old.

Special Application Considerations

Some situations require special approaches:

- Self-employed applicants: Prepare more extensive income documentation, including tax returns for the past two years and recent bank statements showing consistent income.

- Fixed-income borrowers: Provide award letters for Social Security, disability, or pension income, and be prepared to show these benefits will continue for the loan term.

- Recently relocated applicants: Have both your previous and current address information ready, as verification systems might not have updated yet.

- Borrowers with thin credit files: Emphasize alternative data points like rent payment history, utility payments, and bank account standing.

The application process may feel intrusive, but remember: for bad credit loans, lenders need additional assurance you’ll repay. Providing thorough, organized information improves your chances of approval at the best possible rates.

Conclusion

Thriving through bad credit loans requires careful consideration of your financial situation, thorough research of available options, and an understanding of how different loan products may impact your long-term financial health. While bad credit may limit some opportunities, numerous lenders offer viable solutions tailored to various credit profiles. By comparing rates, understanding terms, and choosing reputable lenders, you can find financing that addresses your immediate needs while potentially helping rebuild your credit. Remember to borrow only what you can realistically repay and to use these loans as stepping stones toward improved financial stability and creditworthiness.

FAQs

While requirements vary by lender, many bad credit loan options are available for scores as low as 500-550. Some lenders don’t have minimum score requirements at all but instead evaluate your income, employment history, and other factors in conjunction with your credit history.

Both legitimate and predatory lenders operate in the bad credit space. Safe options usually come from established banks, credit unions, and reputable online lenders who verify your ability to repay and offer transparent terms. Warning signs of predatory loans include extremely high APRs (over 36%), pressure to borrow more than needed, hidden fees, and lack of credit check.

Approval times vary by lender and loan type. Online lenders typically offer the fastest processes, with some providing same-day approval and funding within 1-2 business days. Traditional banks and credit unions may take several days to a week for the complete process.

Yes, if the lender reports to major credit bureaus and you make consistent on-time payments. The loan diversifies your credit mix (a positive factor) and establishes payment history (the most important credit factor). However, taking on debt you can’t repay will further damage your score.

Secured loans require collateral (like a car or savings account) that the lender can claim if you default, resulting in lower interest rates. Unsecured loans don’t require collateral but compensate for increased lender risk with higher interest rates and stricter eligibility requirements.